enrollment

Enrollment challenges likely to persist for U.S. colleges and universities as WICHE releases flat high school graduate projections

Last month the Western Interstate Commission on Higher Education (WICHE) released updated high school graduate projections through 2032 . The report contained the following findings and observations:

- The steady growth in high school graduates that led to significant expansion of higher education in the United States in recent decades is coming to an abrupt halt. While the percentage of graduates grew 30 percent from 1995 to 2013, the number of high school graduates is expected to show virtually no growth for the next seven years.

- Dramatic increases in graduates who are Hispanic or Asian/Pacific Islander will continue. The racial/ethnic mix of high school graduates in the United States will shift significantly toward a more diverse population of graduates fueled primarily by large increases in the number of Hispanic (50 percent) and Asian/Pacific Islander (30 percent) public high school graduates through about 2025.

- Marked regional differences will continue as well. There is significant regional variation, with the Northeast and the Midwest experiencing continuing declines in the number of high school graduates, while the West will see slight increases and the South significant and steady increases. Most notably, the South is the engine of growth for high school graduates.

The enrollment challenges noted in these findings are probably not a surprise to most higher education leaders who are already feeling the impact of weakening student demand. Indeed total enrollment in degree-granting institutions declined by more than 800,000 students between fall 2010 and fall 2014 according to IPEDS. The National Student Clearinghouse, which produces data ahead of IPEDS, has now reported enrollment declines for ten consecutive terms through fall 2016.

Note that these sharp declines have been isolated to the two-year public and the four-year, for-profit sectors. That said, the picture is not much better in the four-year public and private sectors. The last five years produced little growth in the aggregate and this has produced a zero sum game in most parts of the country for these institutions. Said another way, for most schools any gain in enrollment comes at the expense of its competitors because the overall market is exhibiting weak overall demand fueled by the underlying demographics, college participation rates that have leveled, and an improving economy with relatively low unemployment.

It never ceases to amaze me how many higher education leaders, who are generally quite aware of these trends, continue to believe that these market forces do not apply to their own institution. I believe this results from a failure to localize these trends to their own student catchment areas and actually measure the probable impact on their future enrollment levels.

And if your institution largely serves graduate or adult learners, don’t think these enrollment challenges do not apply to you. Today’s high school graduates are tomorrow’s graduate and adult re-entry students. Demography eventually impacts every type of institution. Just ask schools that rely on large transfer populations how the decline in community college enrollments are impacting their overall numbers.

While it is easy to get discouraged by these market forces, at Ruffalo Noel Levitz we know that institutions that take a holistic approach and engage in a sustained strategic enrollment planning process are faring better than those who choose to ignore the realities of the current market.

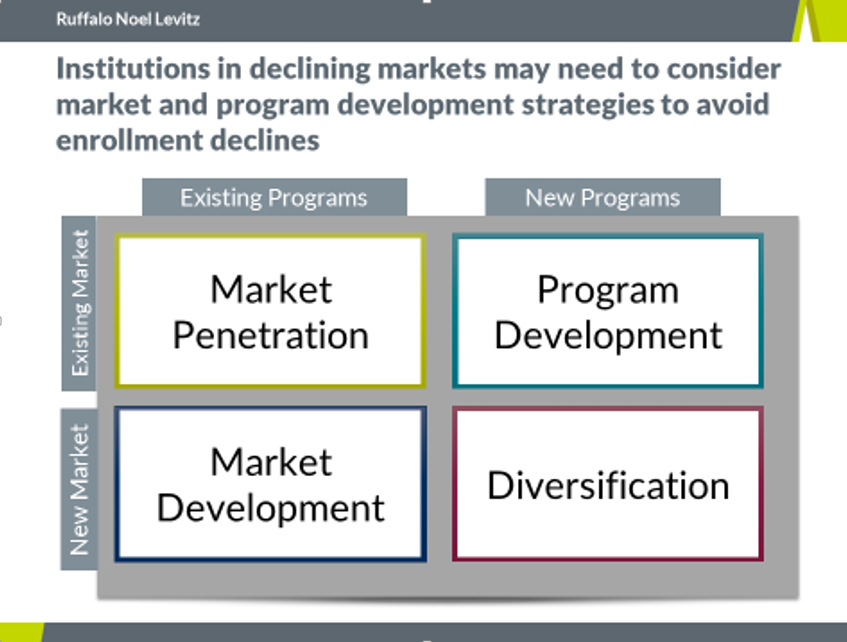

One thing we have learned over the last five years is that schools that take a balanced approach to enrollment strategy development tend to achieve the most success. The following graphic outlines the four broad ways an institution can stimulate additional demand with the intent of either growing enrollment or creating the flexibility to better shape the characteristics of the students they serve.

Historically, higher education institutions have focused on market penetration strategies when they experience uncertainty in their ability to achieve enrollment goals. While it is still important for institutions to rigorously assess their ability to further penetrate existing markets (with their existing programs), in a flat or declining market, gaining share is challenging, especially if the institution has not actually lost market share in recent years.

In our view, strategies that improve market penetration (and this includes improved retention and graduation rates), need to be balanced with a mix of program and market development strategies to achieve optimal demand. Developing new academic and co-curricular programs along with addressing new geographic and demographic markets is essential for most institutions to meet these enrollment challenges and thrive in these uncertain times.

Read our book on strategic enrollment planning

Developing the effective strategy mix I’ve described is best accomplished through a sustained and data-informed strategic enrollment planning process. You can read more about this in the 2nd Edition of our book Strategic Enrollment Planning: A Dynamic Collaboration.

Questions?

If you would like to speak with me personally about your enrollment challenges or strategies, you can reach me by email.

You can also connect with me at our upcoming executive forum: RNL Strategic Enrollment Planning Executive Forum, April 26-27, 2017, in Chicago

My best wishes for success at your institution in the coming terms.